The third installment in the Bold Penguin series on The Evolving Risks of Small Businesses addresses general liability insurance for business.

Contributed by Nicole Farley, Vice President of Carrier Operations at Bold Penguin. As VP of Carrier Operations, Farley works to streamline the small commercial quoting experience for agents and small business owners, working closely with several large enterprise partners and carriers to achieve mutual short and long-term goals and objectives.

The Evolving Risks Of Small Businesses is a six-part educational series crafted to help insurance agents navigate the demands of commercial insurance, brought to you by Bold Penguin. Each month, we will highlight a new timely topic that will discuss the trends and tips of a particular risk to help ensure that business owners’ investments are protected.

March’s focus is general liability insurance for small businesses. In July 2024, the complete complimentary playbook on The Evolving Risks Of Small Businesses will be downloadable at www.boldpenguin.com.

General liability (GL) insurance for business, sometimes called “business liability” or “commercial general liability,” protects against a range of threats that could negatively impact a business’ financial health and viability.

According to the Insurance Information Institute, “A Commercial General Liability (CGL) policy protects your business from financial loss should you be liable for property damage or personal and advertising injury caused by your services, business operations or your employees.” In simple terms, general liability refers to claims that a business has caused harm to another party. In this post, we will explore how agents can address common misconceptions about general liability (GL) risks for small business owners, why claims are on the rise, and strategies to ensure your commercial customers’ investments are protected through general liability insurance for business.

A 2023 survey conducted by NEXT insurance discovered that while GL is the most common type of insurance policy purchased, approximately 50% of respondents did not have any GL coverage at all.

It’s not clear why that 50% do not have this coverage, but it is clear that this makes them extremely vulnerable to loss. This represents an educational opportunity for agents, as trusted advisors to small and medium-sized businesses (SMBs), to make them aware of how general liability insurance for business can help them and why it’s needed to protect their investments.

In a recent interview with Evan Paul, Commercial Lines Underwriting Manager for Westfield, he stated, “Insurance is commonly perceived by business owners as a safety net reserved for major catastrophes. The reality is that the majority of GL claims are relatively small in scale. It's crucial to enlighten insured individuals about the significance of maintaining GL coverage and illustrating scenarios where its practical application is not only conceivable but highly beneficial for all parties involved.”

Becky Monfre, Vice President of Digital Distribution for Coterie Insurance, adds another distinction that agents should be sure to highlight. “We often observe our clients looking for business insurance or liability insurance while not understanding that the intent of this coverage is to cover third-party claims for bodily injury and property damage caused to others. There are a few key exclusions that can be confusing to a policyholder, such as property of others in their care, custody, and control. This insurance is meant to protect our insured against litigation and paying out of pocket, but not cover their own property or their own damages.”

General liability insurance for business covers a lot, but it is just as important to understand and explain to business owners what it doesn’t cover. Agents are cautioned to look for exclusions such as business-related auto accidents, employee injuries/ illnesses, damage to the business property, mistakes in professional services, or illegal acts by the business owner or their employees, to name a few.

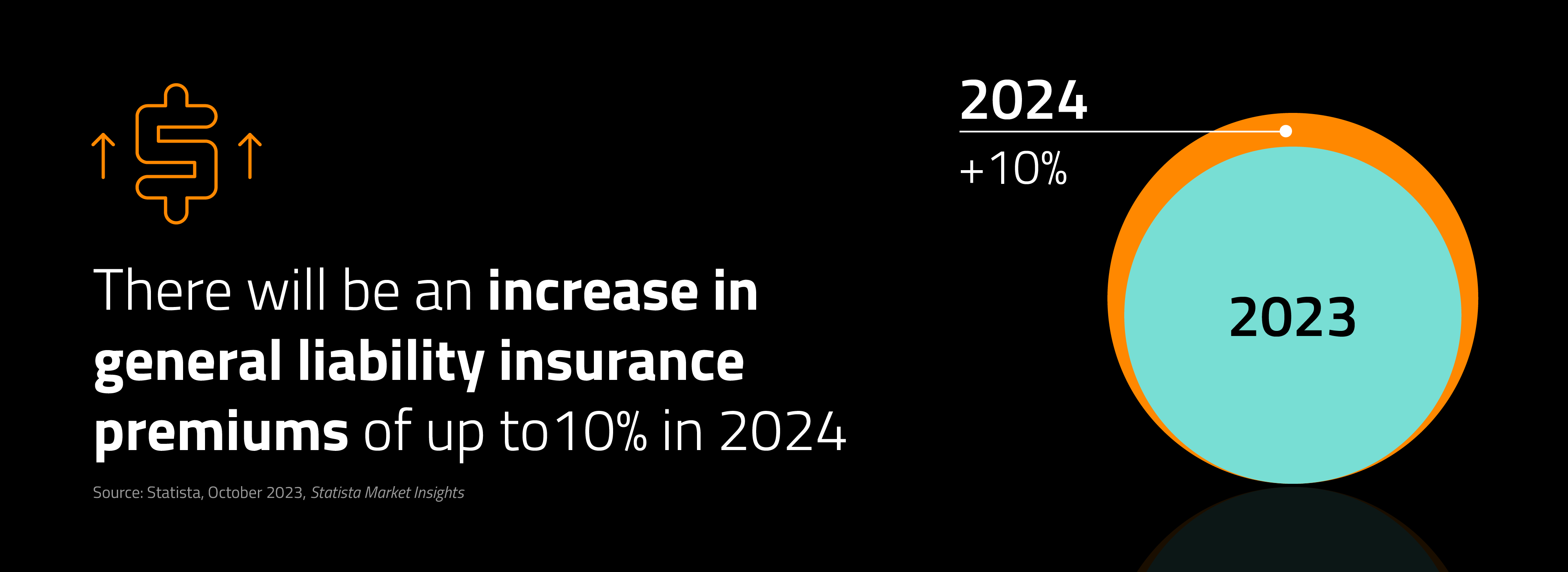

GL usually is not required by law. However, some states include general liability insurance for business in their licensing requirements for construction contractors or developers. It’s important to understand the unique needs of each of your commercial customers to advise them on the right protection. You should review with your customers their contracts, loan documents, and other documents that outlined required insurance coverages and limits that they will need. Just as GL risks don’t look the same as they did 10, 20, or 50 years ago, they will not look the same in the future. General liability risk is not going away. In fact, the opposite is true, according to a recent Statista Market Insights study, there will be an increase in premiums on general liability insurance for business of up to 10% in 2024, with the “most gross written premium generated in the United States, with $179.7 billion in 2024.”

Outlined below are just a few reasons why SMBs, and their commercial insurance agent, should care about this trend and ways to help mitigate these risks.

Our litigious culture contributes to increased risks for business owners. According to a 2021 study on Small Business Statistics by The Zebra, “90% of all businesses experience a lawsuit at some point in their lifespan.”

Customers, employees, and other stakeholders are turning to legal action quicker than ever before, even for minor issues. There are a few relatively easy things to implement to keep these incidents from escalating. Monfre added, “Slip and fall claims are very common. It is important to keep surveillance video of any issues and record incidents as they happen.”

How a commercial agent can help: Advise your SMB customers to implement strong risk management practices like holding general liability insurance for business, and maintain accurate records to mitigate the risk of litigation. Carriers are a great resource for best practices and tips and tricks for small business risk mitigation.

The evolution of GL risk is driven largely by the shift in laws and regulations related to business practices, consumer rights, and workplace safety, which are frequently subject to change.

How a commercial agent can help: Keep abreast of these changing legal developments so you can advise SMBs on how to stay protected and avoid potential liabilities.

Commercial businesses are expected to uphold increasingly high standards in quality of products and services, and overall customer satisfaction. When an SMB fails to meet these expectations, customers are quick to resort to legal actions, with subsequent financial loss to the business. Reputations also can be tarnished easily with the prevalence of social media.

How a commercial agent can help: Advise your SMB customers to invest in quality control processes, customer service training, and proactive communication to manage consumer expectations and reduce the risk of liability claims from dissatisfied customers.

As new industries emerge and traditional industries evolve, so do their corresponding risks. And each of those new risks requires a customized approach to mitigation. Paul continued, “Insureds in various industries face unique exposures that demand a customized insurance approach.”

How a commercial agent can help: Paul advises, “Crafting a policy tailored to the specific nature [and operational risks] of their work not only adds significant value but also fosters long-lasting client relationships.”

Currently, there are several notable patterns in the types of liability claims that carriers are experiencing that agents should be aware of in order to stay ahead of the curve. Monfre states, “In the small business sector we continuously see claims for quality of work, such as walking off the job, a job poorly done, etc. These losses are typically not covered. If you are a small business asking another business to do work for you, the best thing you can do is do a deep dive on the contractor and make sure they are reputable, insured, and have a contract that clearly outlines the work in place.” When choosing a subcontractor, prioritize years in business, whether they are disciplined in the types of jobs they are willing to accept, and strong employee training.

Monfre continued, “[Another] pattern [we] have seen in the past is that insureds often think the issue was not them, or will go away if they are seeing a customer complaint. We would rather our insureds call and inform of a potential claim so we can advise and get involved on day one, rather than after the fact. It is better to have the insurance company, and any defense needed involved in investigating and collecting real-time information, than trying to piece things together later. We recommend [contractors] taking pictures before and after leaving a job site on a completed project.”

There is reason to be hopeful about the future of GL as carriers provide additional support and ease some of the stress currently weighing on SMBs’ liability.

Monfre predicts that “Going forward there will be more value-adds that become an important part of the landscape of the general liability landscape. Clients will want more than a ‘just in case’ insurance policy, but will look to insurance policies that help them proactively manage their risks. Insureds will demand support in avoiding risky behavior and will look to their agents and insurance providers to help them get there.”

Technology will also play a role in adding efficiency by streamlining the entire quote process around general liability insurance for businesses and subsequently could lower insurance costs. Paul continued, “The evolving legal landscape significantly influences the payouts on GL claims, thereby contributing to rising insurance costs. Amid this scenario, a key avenue for positive change lies in the realm of technology. The ongoing integration of technology by insurance carriers holds immense potential, streamlining the insurance purchasing process for insured individuals, carriers, underwriters, and agents alike. This technological advancement is poised to enhance efficiency, reduce operational costs, and, ultimately, contribute to maintaining lower insurance rates for the benefit of insured individuals.”

The evolving nature of GL risk introduces a great educational opportunity for the agents who advise SMBs. When discussing general liability insurance for business, start by disabusing the misconceptions about what it is and why it is needed. Then take a deeper dive into:

Take time to fully understand the unique needs of each customer so you can customize coverage. In doing the above, you will solidify your role as a trusted advisor and give your customers confidence that their investments are properly protected.

The preceding is part three of a six-part educational series on navigating commercial insurance, with the purpose of keeping commercial insurance agents abreast of industry trends. The Evolving Risks Of Small Businesses complete playbook will be available in July 2024 at www.boldpenguin.com.

The fourth installment in the Bold Penguin series on The Evolving Risks Of Small Businesses addresses the changing landscape and need for surety bonds.

Carlos Gonzalez-Avila, Small Business Insurance Specialist at Bold Penguin, provides insights on support for agents in the insurance business in this issue of 3 Questions.